DC struggles to build affordable housing in wealthy neighborhoods. Here’s one reason why.

The Brooks short-term housing shelter in Ward 3. Image by Chelsea Allinger, used with permission.

This is the fourth in a series of posts about how affordable housing works, by an affordable housing developer. This post explores the mismatch between the timelines for accessing affordable housing financing and land acquisition, which creates unintended barriers to development, especially in areas where land is more expensive. Read the rest of the series here.

What does comedy have in common with affordable housing? The secret ingredient for both is timing.

At the start of her second term in 2019, Mayor Muriel Bowser unveiled an ambitious plan to build 36,000 housing units in the District, including 12,000 income-restricted, subsidized homes, by 2025. This plan was part of a broader regional initiative led by the Metropolitan Washington Council of Governments (MWCOG) to build 320,000 housing units by 2030 in order to address the region’s housing shortage. In addition to answering the call from MWCOG, Bowser published a Housing Equity Report in October 2019 that broke the 12,000 affordable unit goal down into specific targets for each of the District’s planning areas.

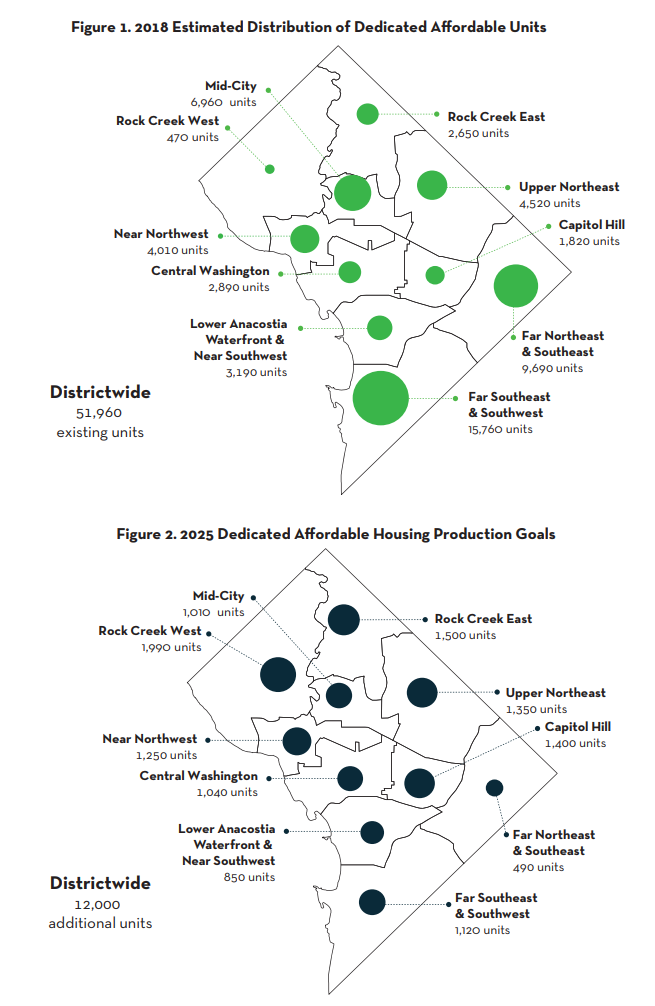

The purpose of these more specific targets was to reverse historical patterns of segregation and exclusion by creating quantifiable affordable housing production goals for wealthy, predominantly white neighborhoods such as Georgetown, Dupont Circle, Capitol Hill, and in particular communities west of Rock Creek Park. The below maps from the Housing Equity Report illustrate the distribution of income-restricted, subsidized units in the District as of 2018 (top) and the production goals for income-restricted, subsidized units from 2019 onward (bottom), with a clear emphasis on a more balanced geographic distribution:

Source: District of Columbia Office of Planning, “Housing Equity Report,” 2019

Since 2019, the District has made considerable progress in reaching both the 36,000-unit and 12,000 income-restricted, subsidized-unit goals. Through February 2024, developers in DC have produced 33,661 total units (94% of the target) and 9,230 affordable units (77% of the target). Yet the most affluent parts of the District are still lagging well behind their specific targets. Neighborhoods west of Rock Creek (“Rock Creek West”) have produced a mere 135 affordable units, or 6.8% of their target. Capitol Hill has produced 321 affordable units, or 22.9% of its target. Georgetown, Dupont Circle, and Logan Circle (“Near Northwest”) have produced 329 affordable units, or 26.3% of their target.

Meanwhile, by contrast, neighborhoods east of the Anacostia River have produced 3,539 affordable units, 220% of their target. Despite the well-intentioned goals of the Housing Equity Report, the production of income-restricted, subsidized housing in the District continues to be deeply uneven geographically, with such homes mostly absent from wealthy white neighborhoods and heavily concentrated in low-income black neighborhoods. Despite DC policymakers’ big push to build 12,000 income-restricted, subsidized units within five years, the de facto residential segregation of our city continues.

Why has the implementation of the Housing Equity Report failed to move the needle more significantly? Often, policymakers focus on cost. Because land values are higher in wealthy areas, building affordable housing in those areas is more expensive. This is certainly true, yet the District has demonstrated a willingness to prioritize funding for projects in these areas despite higher land costs, precisely in order to meet its geographic distribution goals. Observers also focus on political opposition, since residents rich in money, or time, have in many notable instances organized to try to block new housing, whether market-rate or affordable, in their neighborhoods. This is also certainly true, yet there is now considerable political will in the District, including from the mayor, DC Council, and many Advisory Neighborhood Commissions, to support such projects.

The District’s experience in the five years since the release of the Housing Equity Report demonstrates that funding and political will are not the only obstacles to equitable distribution of affordable housing. The real impediment that we still have to reckon with is time. As this column will explain, there is an enormous disconnect between the time it takes to assemble the funding sources needed to build affordable housing and the time available to purchase land in a strong real estate market. Without addressing this specific challenge, District policymakers will not make meaningful progress toward achieving the goals of the Housing Equity Report.

Affordable housing development moves slowly, and land acquisition is challenging

Building a new building is often a slow process. Real estate developers have to identify land, negotiate a purchase contract with the seller, fully design the building, secure permits, and close on financing (both debt and equity) in order to begin construction. Affordable housing developers navigate all of these challenges, with an additional twist: The funding sources they rely on are generally allocated through a competitive process managed by government agencies, which in practice means it takes an especially long time to close on financing. In my previous column on the District’s Housing Production Trust Fund, I explained how it often takes three to four years from a project’s start to securing construction financing, which is significantly longer than the one to two years it usually takes for a market-rate project to do the same with conventional debt and equity.

In a strong real estate market, sellers do not want to wait for three to four years for a sale to close, and will insist on a shorter time period. This requires the buyer to come up with an interim acquisition financing strategy to buy and hold the land while waiting to complete design, permitting, and assembly of construction financing sources. This interim acquisition phase is challenging for two reasons: It is expensive and it is risky.

Interim acquisitions are expensive because they usually cannot support much debt, so the purchaser must contribute a large amount of cash to buy the property. For example, consider a hypothetical vacant piece of land in an affluent neighborhood worth $10 million. Because the land is vacant, it does not generate income; in fact, it operates at a deficit because the owner of the land still has to pay some ongoing expenses such as property taxes and insurance. Unlike a fully built and leased building, which produces stable income and therefore can make regular mortgage payments, this property cannot support any debt. Thus, any bank loan the buyer obtains to help buy the lot will be considered a “land loan,” which is based on what the land is worth, rather than the income stream from a building on it.

Land values can fluctuate dramatically with macroeconomic conditions, as even small changes in rents, interest rates, and construction costs can cause large swings in land values (I’ll explain this further in a future column on land valuation). Banks, which are generally risk-averse, thus like to limit their exposure to a potential drop in land values by limiting any loan to a low percentage of a property’s appraised value. In this example, we can assume the bank is only willing to provide a land loan of 50% of the land’s value, equal to $5 million. This means the purchaser must come up with an additional $5 million to buy the property.

In addition, the bank will often require the purchaser to pre-pay interest for the term of the loan by fully funding an “interest reserve” account upfront. If we assume the interim acquisition period is three years, and the bank interest rate is 7%, a fully funded interest reserve would cost $5 million * 7% * 3 = $1,050,000. If we add in closing costs, as well as an operating reserve to cover the property’s deficits, the total amount the developer must come up with is approximately $6.7 million.

Now we get to the risky part. There are a litany of unexpected challenges that can arise in the three- to four-year window that might derail a project: a change in macroeconomic conditions, such as increased construction costs or interest rates; a decrease in government funding availability; an unexpected issue during the design or permitting process; or the emergence of local opposition and threats of frivolous, but time-consuming, lawsuits. If a project is delayed, it can simply run out of time. The bank will eventually insist on having its loan repaid or the interest or operating reserves will run out of money, requiring the developer to contribute additional cash to stay afloat. In this circumstance, the path of least resistance is often for the developer to give up on the project and sell the land to minimize losses and repay the loans.

Without solving land acquisition, the status quo reigns supreme

Affordable housing is not being built in wealthy areas of the District because it is nearly impossible for developers to acquire land there. To build income-restricted, subsidized housing, developers have to come up with large sums of money to invest in high-risk, illiquid assets with a ticking clock. It should come as no surprise that most choose instead to pursue less risky projects.

This is why most affordable housing projects in the District, and in cities across the country, often fall into one of these three buckets:

- Acquisition of property in low-cost areas with weak housing markets. Sellers in such markets have fewer options and are more willing to entertain a long contract period. This is more financially feasible, but it continues to concentrate income-restricted, subsidized housing in low-income neighborhoods, and does little to disrupt entrenched patterns of racial and economic segregation.

- Pursuing redevelopments on publicly-owned land where there is no need for an interim acquisition. This poses less risk for the developer, but opportunities are limited as most land, particularly in affluent neighborhoods, is privately, not publicly, owned.

- Focusing on affordable housing preservation projects. This generally entails acquiring an existing, income-producing property that can support debt. In addition, special government-backed financing programs, such as the District’s Affordable Housing Preservation Fund, help cover interim acquisition costs for preservation projects. However, this has limited impact in affluent neighborhoods as there is little income-restricted, subsidized housing there to begin with.

These types of projects all have merit, but they cannot and will not enable the District to achieve the goals stated in its Housing Equity Report. The entire purpose of the report was to disrupt the business-as-usual mindset of affordable housing development in the District and establish a new paradigm based on a balanced geographic distribution of projects. But setting a goal without creating tools to accomplish it is a dead end.

If we do not solve the interim acquisition challenge, we will never make meaningful progress in building affordable housing in affluent neighborhoods of the District and dismantling our deeply entrenched lines of segregation.

How a revolving acquisition fund could have a transformative impact

To actually create a pipeline of income-restricted, subsidized housing in its affluent neighborhoods, the District should establish a fund that can specifically be used for interim land acquisitions in communities that have not met their Housing Equity Report targets, such as Chevy Chase or Dupont Circle. Affordable-housing developers would pay the fund back with interest upon securing construction financing, which would allow the funds to be recycled into new projects. This is similar to how the Housing Production Trust Fund works for construction financing, where funds are recycled after the building is constructed and in operation. The good news is that District policymakers do not need to start from scratch to implement this concept, as they already have an existing tool they can repurpose for this use, the Site Acquisition Funding Initiative (SAFI) program.

SAFI was created in 2005, several years after the Housing Production Trust Fund received dedicated funding from the District’s deed and recordation tax revenue. The program’s original purpose was to support projects needing interim acquisition financing prior to closing on construction financing. From its inception, SAFI has been limited to nonprofit developers only, with a heavy emphasis on projects that would preserve existing affordable housing. While the program still exists today, it has been surpassed by the District’s Affordable Housing Preservation Fund, which is similarly focused on preservation projects but is open to both nonprofit and for-profit developers.

SAFI is currently designed for very small projects. Loans are capped at $3 million and structured as regular mortgages, which means they cannot be combined with a bank’s land loan, since they take the land loan’s place. This is different from the Affordable Housing Preservation Fund, which provides subordinate loans (also known as “second mortgages”), allowing it to be paired with a land loan to more fully fund interim acquisition costs. Land values in DC have recently averaged $100,000 per unit, so a $3 million loan on its own would support the acquisition of land for a 30-unit project. In the case of our hypothetical $10 million vacant piece of land, a $3 million SAFI mortgage that cannot be combined with any other loans is not of much use; in fact, it is less than the $5 million land loan that a bank would likely lend an affordable housing developer.

However, if SAFI adopted similar terms to the Preservation Fund, such as allowing loans to be a subordinate mortgage with a cap above $3 million, it could provide, for example, a $4 million second mortgage to be combined with the $5 million land loan. Together, this would provide $9 million in interim acquisition funding, requiring the affordable housing developer to contribute $1 million as a down payment in addition to funding any required interest reserves and closing costs. This would make it feasible for affordable-housing developers to more routinely acquire land in high-opportunity neighborhoods to build income-restricted, subsidized housing without taking on risk and expenses that exceed their constraints.

Both SAFI and the Affordable Housing Preservation Fund are managed on behalf of the DC government by professional, third-party lending partners known as community development financial institutions (CDFIs). CDFIs focus on providing financing for underserved or low-income neighborhoods and come in a variety of forms, including credit unions, minority-owned banks, and community development corporations. Some of the most established CDFIs today are non-profit loan funds that arose out of post-1968 Fair Housing Act efforts to combat redlining and other discriminatory lending practices. These funds often specialize in managing lending programs on behalf of local governments and other agencies for initiatives like affordable-housing projects or small-business growth. CDFIs already play a crucial role in the District’s affordable housing development ecosystem, and are well-equipped to manage any new interim acquisition funding program for high-opportunity neighborhoods.

With any lending program, it is pivotal to carefully manage risk. When banks make risky loans that they cannot recoup at a grand scale, the entire global financial system can collapse, as in 2008. As I discussed earlier, there are numerous hurdles that can arise during the interim hold period. Lenders must carefully vet any interim acquisition loans to assess criteria such as the project’s likelihood of paying off the loan by securing the necessary construction financing, the borrower’s ability to actually build the project, and the borrower’s financial capacity to make payments on the loan if anything goes wrong. Lenders should also maintain minimum down-payment requirements to ensure borrowers have “skin in the game” and borrower-lender incentives are fully aligned. Lenders must also manage overall portfolio risk to regularly assess how vulnerable the entire fund is to changes in macroeconomic conditions.

For an interim acquisition loan program to be successful, it must be well-managed with thorough, careful underwriting that avoids undue risks. This is especially true for a program where the government is stepping in to fulfill a need that is currently not being met by the private market. Often, the market avoids lending money for a reason; prudence is always required when there is an existing perception of high risk.

An alternative approach is for the government to directly acquire land. However, if the government pays the full cost to acquire a property up front, rather than leveraging private capital from banks and affordable-housing developers, it might get less bang for its buck. The government could spend $10 million to buy our hypothetical vacant lot. Alternatively, it could lend $2 million to a CDFI, which (assuming a 1-1 public to private leverage ratio) could combine that public money with $2 million in private money to make a $4 million loan. That $4 million loan would then be combined with private bank money (the land loan) and the developer’s equity (down payment) to produce the same result at a fifth of the cost to the government. To solve this problem at scale, it is therefore more prudent—if a government is looking to be conservative with its money—to leverage private capital to generate more funding overall, allowing more projects to move forward.

Another alternative would be for the government to purchase land by issuing bonds secured by the property, which is another form of utilizing private debt financing. This strategy, however, only works when the government has spare bonding capacity, which the District currently does not. Often the argument to prioritize direct government purchase of land is based on an ideological preference to promote the public over the private sector. But, if government funds are limited—as they are in the District’s current budget environment—forsaking the role of private capital will result in fewer projects. A CDFI-managed, government-supported acquisition fund could be an effective model of public-private partnership, as is already the case with the District’s Affordable Housing Preservation Fund.

Despite the challenges, the District has the ability to live up to the vision outlined in Mayor Bowser’s Housing Equity Report. Building dedicated affordable housing in historically exclusive and affluent areas of the city is a long-overdue mission, and one that would finally fulfill the District’s obligations under the 1968 Fair Housing Act to meaningfully desegregate its neighborhoods. District policymakers and residents have demonstrated a shared commitment to this goal. It is time to start turning that goal into reality, and the District can begin by establishing a land-acquisition program.