What HQ2 could mean for the Washington region’s housing market, in seven charts

Image by Erin used with permission.

This feature originally appeared on urban.org and is part of Urban-Greater DC, an initiative to inform policy debate and decision-making to address persistent inequalities and improve economic mobility and access to opportunity in the District of Columbia and the Washington region.

The Washington, DC, metropolitan area economy has expanded steadily over the past two decades, although since the Great Recession, it has lagged behind many other large US metropolitan areas. The region’s prosperity has attracted more residents, expanding the population from 4.8 million in 2000 to an estimated 6.2 million in 2017.

But in recent years, housing production has not kept pace with population growth, and home prices and rents are climbing in most communities.

Many households spend an excessive fraction of their income on housing, putting pressure on family budgets and forcing many to trade short commutes for more affordable housing options. Although the brunt of the housing affordability challenge falls on low-income households, households with moderate and middle incomes are increasingly feeling the squeeze.

These challenges could intensify if the Washington area’s recent slow-growth trajectory accelerated with the arrival of a major employer and tens of thousands of new jobs. The Metropolitan Washington Council of Governments (MWCOG) estimates that the region needs 235,000 more housing units by 2025 just to keep pace with expected job growth. An additional 50,000 new jobs could push that production target for the MWCOG region to around 267,000, requiring a pace of housing production substantially above current levels, which is expected to produce only about 170,000 new units by 2025.

To respond effectively, the region needs to understand today’s challenges. The current housing shortfall reflects the slowing of housing production in recent years. If jurisdictions return to higher rates of new housing construction while crafting policies that preserve existing affordable homes and protect residents, the region can support a well-functioning housing market and meet the needs of households across the income spectrum.

Here, we provide a starting point for conversation about how to realize this goal: seven charts that tell the story of the Washington area’s recent growth and housing market trends.

These charts provide current and historical data for the whole metropolitan statistical area (as defined by the Office of Management and Budget) and for the “inner region,” which includes the District of Columbia, five counties (Arlington, Fairfax, Loudoun, Montgomery, and Prince George’s), and three cities (Alexandria, Falls Church, and Fairfax).

1. Expanding job opportunities have fueled the region’s growth

The past two decades have brought robust job growth to the region. However, the number of jobs increased little during the Great Recession, and the pace of growth still has not returned to prerecession levels. In fact, employment growth since 2012 has fallen short of the national growth rate.

Nonetheless, 169,000 new jobs have been added to the metropolitan economy in the past five years. More than three quarters of this growth has occurred in the inner region, which gained 131,000 jobs between 2012 and 2017.

The region’s unemployment rate is only 3.2%, and labor force participation rates are high. But wage growth has been flat since 2010, leaving many people struggling to get ahead.

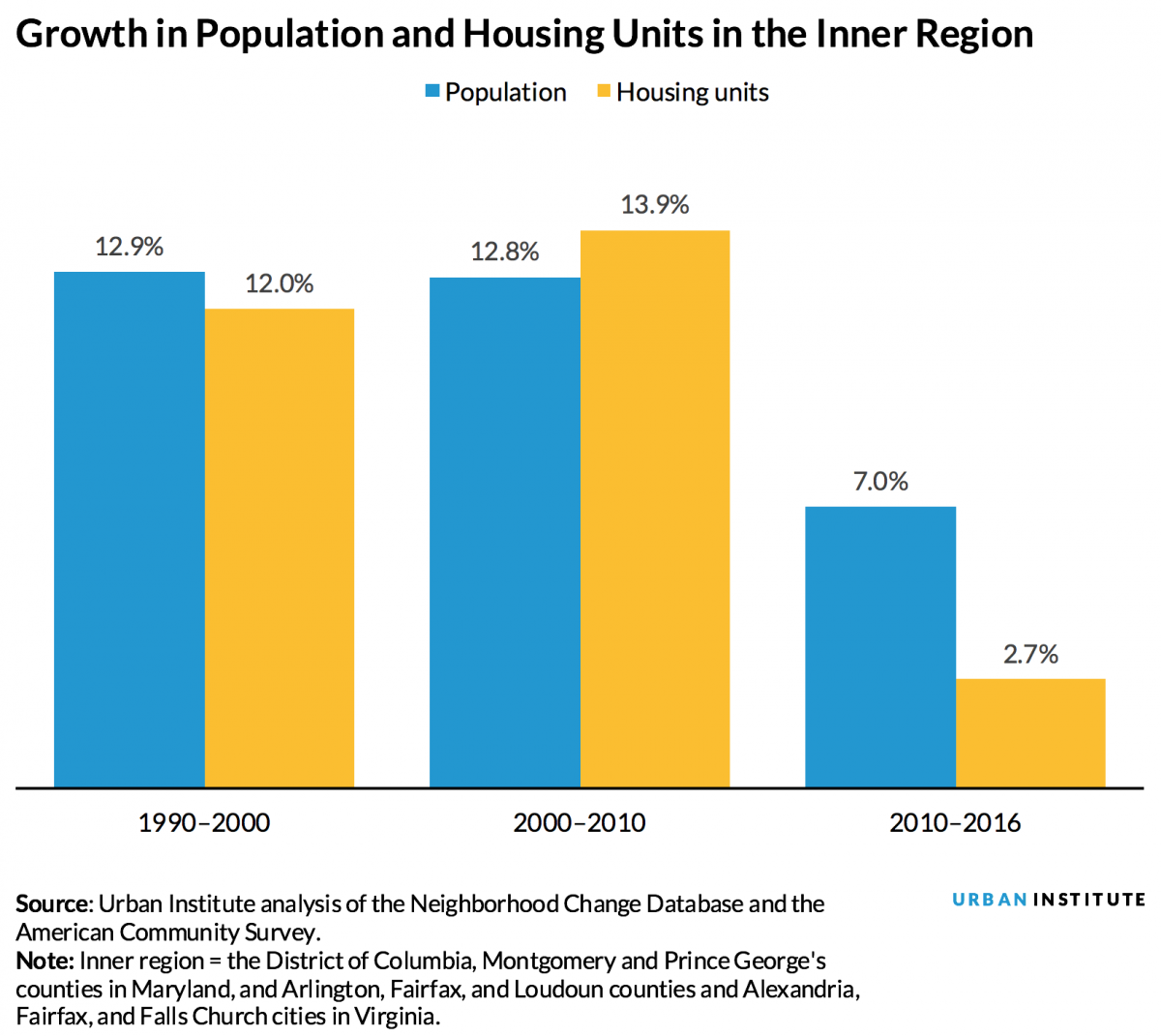

2. Housing units have not kept pace with population growth

Fueled by healthy job growth, the Washington region has also experienced rapid population growth. Between 2010 and 2016, the metropolitan area grew 9.1%, compared with 5.8% population growth among the nation’s 10 biggest metropolitan areas*. And more than half the metropolitan area’s recent population growth occurred in the inner region.

Until recently, housing production kept pace with population growth. But since 2010, housing production has fallen short. While the inner region’s population increased 7%, the number of housing units increased only 3%.

With the shortfall in production, housing vacancy rates have dropped for both rental and for-sale housing. As of 2012–16, the rental vacancy rate for the inner region stands at 5.0%, and the vacancy rate for for-sale housing is 1.1%.

* Including Washington, DC, the 10 biggest metropolitan areas by population are New York City, Los Angeles, Chicago, Dallas, Houston, Miami, Philadelphia, Atlanta, and Boston

3. The region’s population is growing fastest at the top of the income ladder

Average household incomes (adjusted for inflation) have climbed steadily since 2000, with the inner region slightly outpacing gains for the metropolitan area.

This overall increase masks a significant shift in the mix of households at different income levels. The number of households in the middle of the income spectrum remained essentially unchanged, while the number of low-income households increased less than 20%. Flat wages might be contributing to the lack of growth in the number of middle-income households.

In contrast, the number of households with incomes above $150,000 grew 34%, with the number of renters in this income bracket jumping 59%. This rapid growth in the number of households with high incomes can happen when existing residents move up the income ladder and when new, high-income residents move to the region.

Along with the shortfall in housing production, the surge in high-income households puts upward pressure on house prices and rents, making it more challenging for both low- and middle-income households to find housing they can afford.

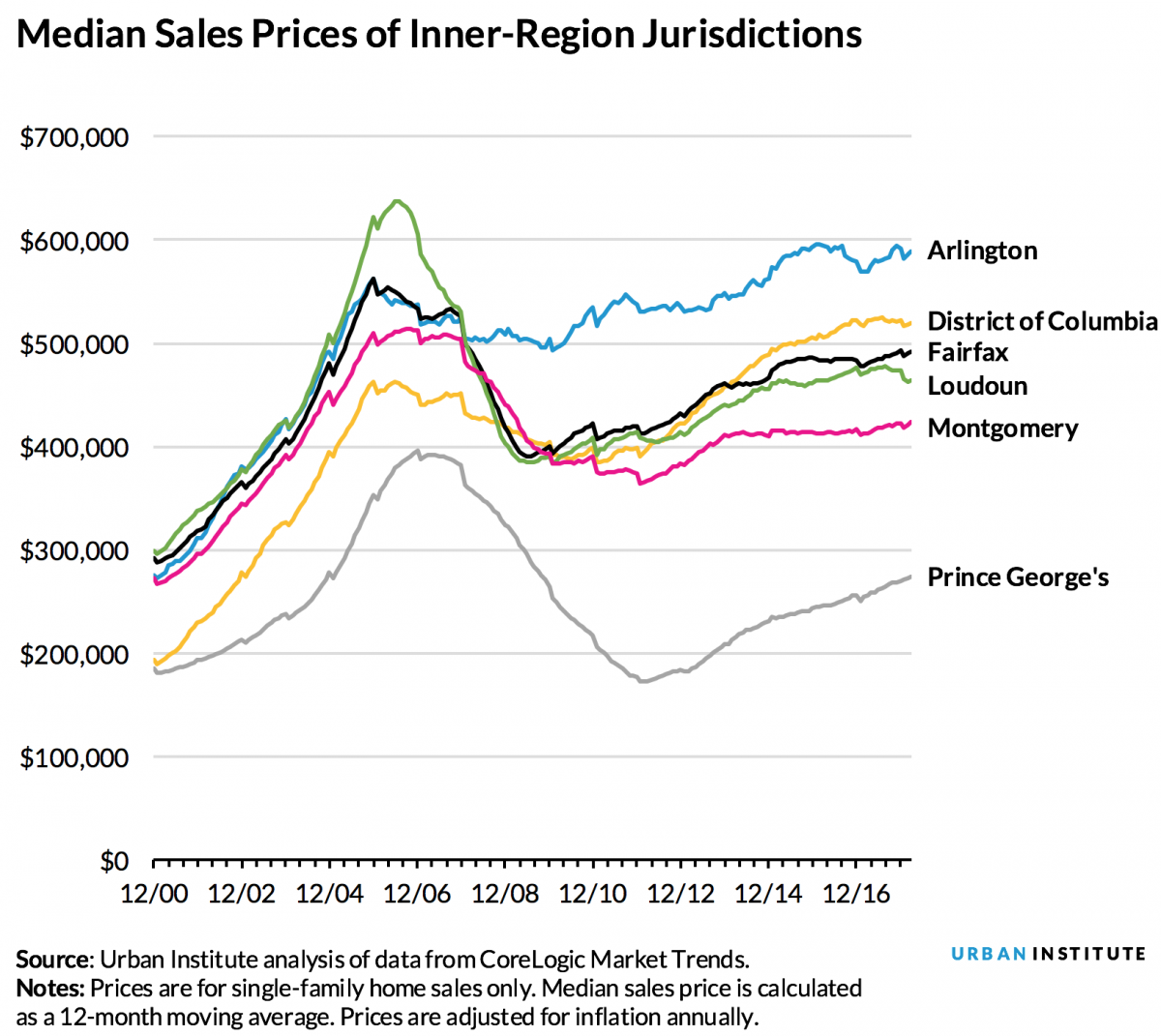

4. Rising demand has pushed up house price

House prices have been climbing steadily (even after inflation) in most of the region since 2010, particularly in Arlington County and the District of Columbia, where median sales prices now surpass $500,000. Together, rising incomes and the shortfall in housing production put upward pressure on house prices across the inner region.

These prices are increasingly out of reach for many of the region’s middle-income workers, based on wages they can earn working full-time in such occupations as nursing, public safety, and administrative support.

But housing market trends vary across communities. The District of Columbia has seen its median sales price climb from close to the lowest in the region in 2000 to the second highest in 2017. In contrast, Prince George’s County suffered the biggest decline in the Great Recession and experienced the slowest recovery.

Strategies for managing the region’s housing market pressures will need to be tailored to the differing circumstances of individual jurisdictions.

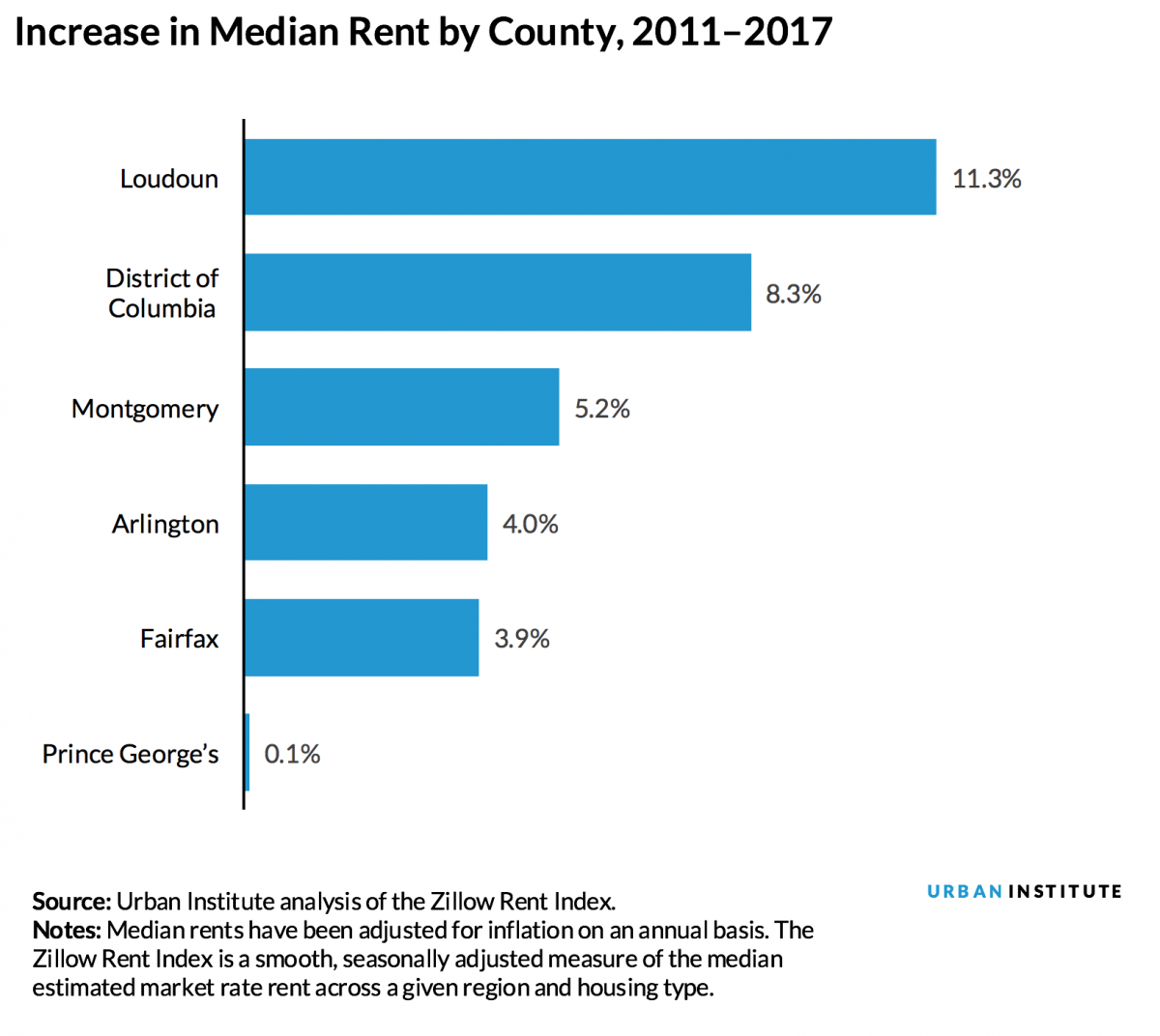

5. Rents have been steadily increasing across the region

Renters, who can be especially vulnerable to rapid changes in the housing market, have seen steep rent increases in many parts of the region.

Rapid growth in the number of high-income renter households drives these increases, which have been especially dramatic in Loudoun County and the District of Columbia. Between 2011 and 2017, rents in Loudoun shot up 11% and climbed 8% in the District of Columbia.

Rents, like house prices, are considerably lower in Prince George’s County than in other inner-region jurisdictions. And the average (inflation-adjusted) increase in rents for the region as a whole, 3.8%, falls short of most other large metropolitan areas, including San Francisco and Seattle, Houston, and Atlanta.

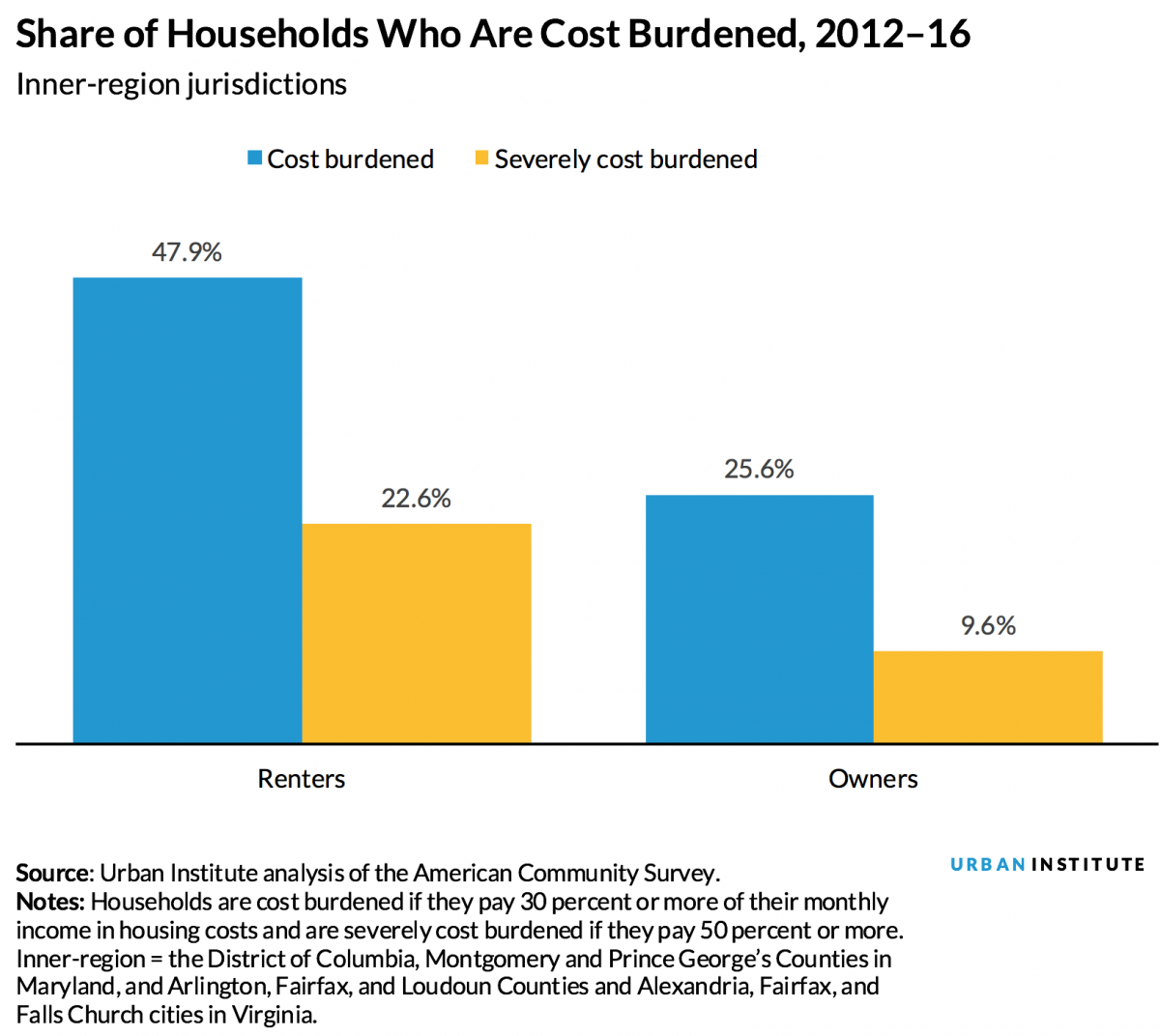

6. Many pay a large share of their income for housing

Because of high costs, many renters and homeowners have to devote unaffordable shares of their income to housing.

Almost half of renters and a quarter of homeowners in the inner region pay 30% or more of their income on housing, a share that the US Department of Housing and Urban Development considers unaffordable. And 23% of renters and 10% of homeowners are severely cost burdened, meaning housing eats up at least half their income.

The share of cost-burdened renters in the inner region has stayed about the same over the past 12 years, while the share of cost-burdened homeowners has fallen from 35% in 2008.

Most large US metropolitan areas have even more severe housing affordability challenges. And low- and moderate-income households bear the brunt of the affordability challenges.

Among households with incomes below 80% of the area median ($70,150 for a family of four), 80% of renters and 73% of owners have unaffordable cost burdens. And George Mason University has projected that the Washington metropolitan area will add 149,000 households with incomes below 80% of the area median by 2023.

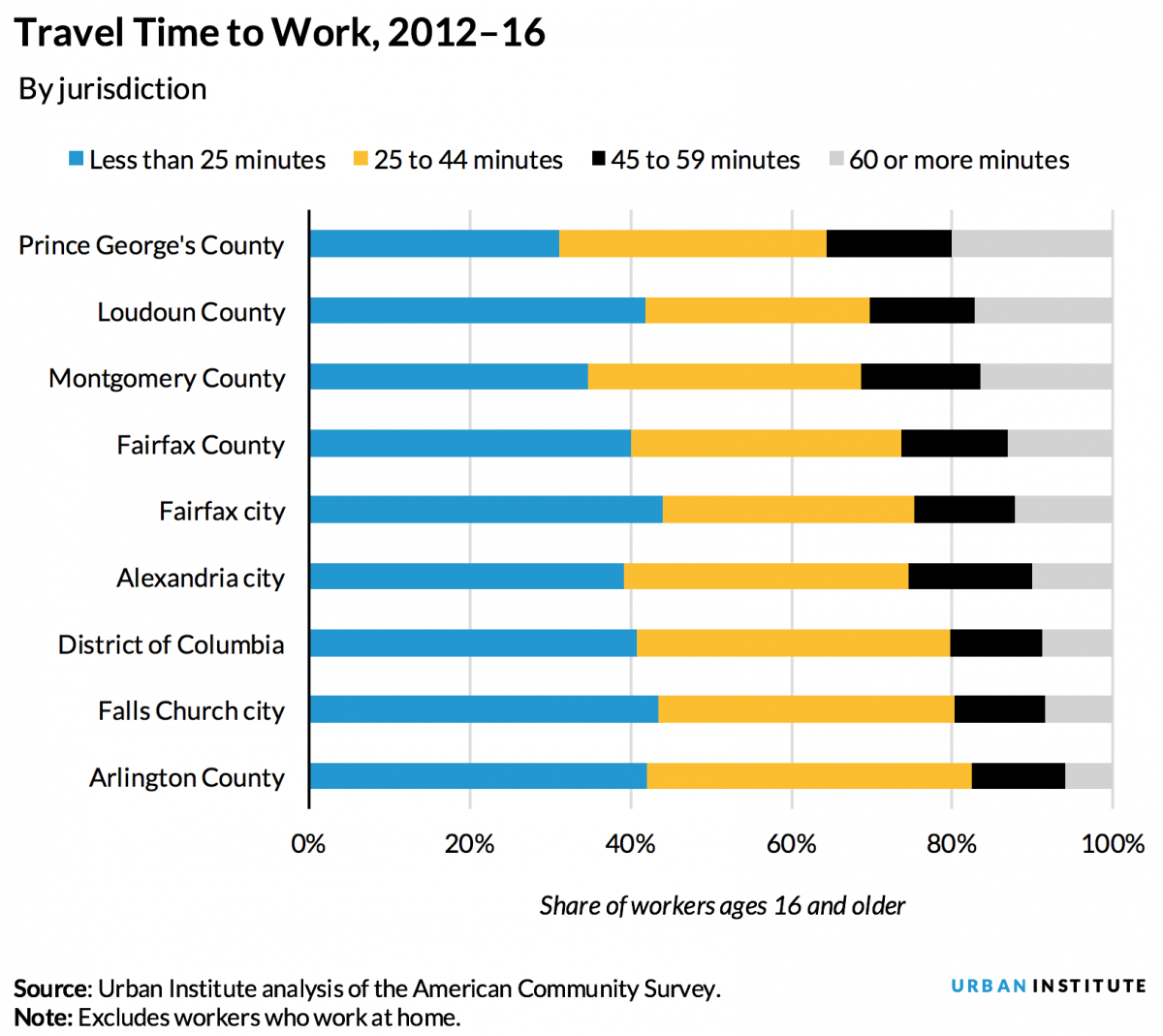

7. Workers trade short commutes for affordable housing

Rising housing costs, particularly near job and transit centers, have forced many to seek cheaper housing options in other areas. But this sometimes lengthens their commuting times.

Places with low housing costs, such as Prince George’s County and Loudoun County, have long commuting times for workers, with 20% of Prince George’s County workers traveling more than an hour to get to work, compared with only 6% in pricier Arlington County.

This presents a challenge to the region in improving the quantity and quality of transportation options, as well as balancing the locations of job centers with housing that serves the full income spectrum.

So does this tell us about the impact could Amazon have?

The arrival of a major new employer, such as Amazon HQ2, would increase pressure on the DC region’s housing market. Without substantially more housing production at a wide range of rent levels and price points, the challenges of rising affordability pressures and lengthening commutes will intensify, and more households will experience hardship.

But since the Great Recession, the Washington area has shown tremendous resilience, and many leaders in the public, private, and nonprofit sectors are focused on housing affordability. Ongoing conversations are addressing what it would take to boost the pace of new housing production in communities throughout the region, and local jurisdictions are exploring various planning and policy options.

Although the region’s housing affordability challenges warrant serious concern, they can be addressed by a coordinated and committed effort by our entire region before they reach the extremes confronting the nation’s highest-cost markets.

Working together, the jurisdictions that make up our region have the capacity and resources to respond to accelerated job and population growth, strengthening the housing market so it better meets the needs of households across the income spectrum.

Whether they do so will go a long way toward determining whether we are building a prosperous and inclusive region for all our residents.

Project credits:

RESEARCH: Leah Hendey, Peter A. Tatian, Margery Austin Turner, Bhargavi Ganesh, Sarah Strochak, and Yipeng Su.

DESIGN: Christina Baird

DEVELOPMENT: Ben Chartoff

EDITING: David Hinson

Correction: A previous version of this story mistakenly said that 50,000 new jobs would push the region’s housing production target above 275,000 units. The correct number is around 267,000 units for the Metropolitan Washington Council of Governments region. We also corrected the sentence to say that current levels of housing production are expected to produce only about 170,000 new units by 2025 instead of by 2026 (corrected 11/5/18).