We give some millionaires $22k/year in housing assistance. Weird, right?

Image by CafeCredit.com licensed under Creative Commons.

We often think about housing subsidies as money the government gives to low-income people to help them pay for a place to live. But the US actually gives far more housing aid via the tax code through deductions that go mainly to the country’s highest earners.

In particular, the $77 billion Mortgage Interest Deduction (MID) is a wildly inequitable program, delivering the lion’s share of its benefits to those making more than $100,000 per year.

In a nutshell, tax deductions like the MID reduce your total taxable income — for example, if you made $50,000 last year but paid $10,000 in mortgage interest, your actual income for the purposes of calculating your taxes would be $40,000. This is different from a tax credit, which reduces the actual taxes owed.

Here's a refresher on how the MID fits with other housing assistance the government gives, from a post on the subject that I co-authored back in August:

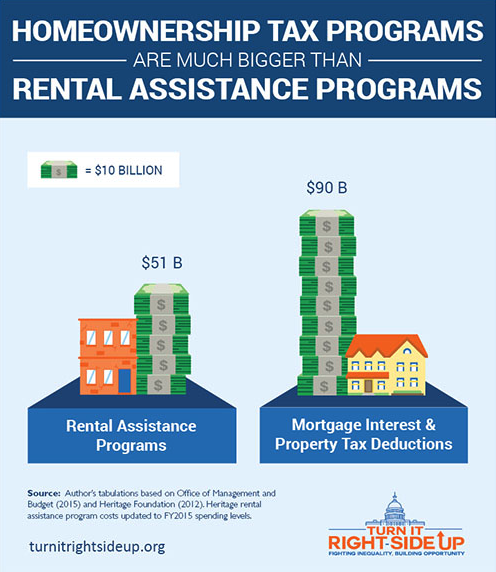

Congress supports housing in two main ways: rental assistance programs and homeownership tax programs. In 2015, the price tag for federal rental assistance programs—which includes Section 8 housing vouchers, public housing, Homeless Assistance Grants, and other programs—was $51 billion. In contrast, two of the largest homeownership tax programs—the Mortgage Interest Deduction and the Property Tax Deduction—cost $90 billion in 2015. That’s nearly double the amount spent on public benefit housing programs.

Because these programs operate through the tax code, they tend to fly under the radar and are thus harder to change. Though they are technically “foregone revenue,” experts and policymakers on all sides of the political spectrum still consider such programs spending, and they should be treated as such.

With tax reform on the Trump Administration’s radar, there are increased calls for reforming the Mortgage Interest Deduction. Many of these reforms, like the three outlined in a recent report from the Tax Policy Center, would make the program more equitable as well as push it closer to accomplishing the stated goals of supporting homeownership.

Why the MID needs reform

The MID is currently projected to be a $96 billion program by 2019. And as we recapped in that earlier post, nearly all of that spending goes to high-earners with large mortgages:

Image by CFED used with permission.

This staggering inequity is because of how the benefit is designed. You can only claim the deduction if you itemize your expenses, something that only those with higher incomes tend to do. As a result, the value of the benefit actually goes up as your income rises. This means that the MID actually incentives mortgage debt, rather than homeownership — you get a larger benefit if you have a more expensive mortgage.

As a result of all these policy design choices, someone making millions of dollars a year — even if they have multiple homes — gets an average of $1,236 per month from the MID. That could cover most or all of a month’s rent for low-income households, whose average share is just eight cents, if they can get the benefit at all.

For someone with a $1 million mortgage, the MID means that the federal government gives you back about $22,000 a year — enough to push a family of three above the poverty line.

Back in 2006, Roger Lowenstein at the New York times summarized the opinion of nearly every economist: “If you eliminated the deduction tomorrow, America would have the same number of homeowners.”

Potential for Reforms

The mortgage interest deduction was once considered a third rail of politics. It’s supposed goal — to encourage and reward homeownership — aligns well with goals of policymakers and the public. However, experts and policymakers from all sides of the spectrum are taking a closer look at the policy, and it seems more likely that something will now change.

Tax reform is of the stated priorities of the new administration and Republican-led Congress. If and when it comes up, it seems likely that the Mortgage Interest Deduction — one of the largest tax expenditures in the federal budget — will be on the agenda, if not the chopping block.

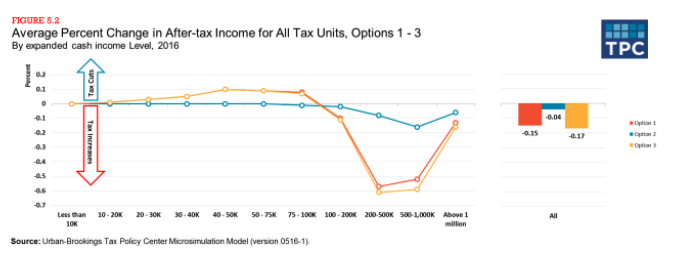

The Tax Policy Center, a joint venture between the Urban Institute and the Brookings Institution, recently released a report analyzing three proposals for reforming the deduction: replacing it with a 15% non-refundable credit, capping it to mortgages at or below $500,000, or a combination of the two.

The good news is that all three proposals would make the program more equitable. The image below shows how the change in average income by income group; the red line is the 15 percent credit, the blue line is the deduction cap, and the yellow line is the combined reform. All of the proposals, but particularly 1 and 3, would reverse but not eliminate the upward redistribution of the current MID.

Image by Urban-Brookings Tax Policy Center used with permission.

Unfortunately, reform could be bad news for our region

One interesting wrinkle of the report is how reforms would impact homeowners by state. Because of higher housing costs — and therefore, larger mortgages — DC, Maryland, and Virginia, would see some of the highest average tax increases of any state. However, this is true of all states with higher average incomes, like New York and California.

Despite that, as renters and homeowners alike struggle with skyrocketing housing cost burdens, a more equitable mortgage interest deduction would be a huge relief to many homeowners in our area.

Other options for tackling the MID

The three proposals outlined in TPC’s report are by no means an exhaustive list. That $77 billion could be used for a lot of things. If we truly want a program that helps more people become homeowners, we might look to bring back the first-time homebuyers credit, a fully refundable tax credit that only lasted from 2008-2010.

We could also use some of the funds to create a credit for renters, who are increasingly seeing staggering affordability crises. At the federal level, housing policy and homeownership policy have often been one and the same, with renters often left to fend for themselves. This is often justified by pointing to the proven benefits of homeownership, like wealth-building and having a stake in neighborhood strength, but at a certain point the plight of many renters can’t be ignored.

What looks increasingly likely, however, is that any Republican tax reform would mostly kill the Mortgage Interest Deduction — perhaps without meaning to. If the standard deduction for a married couple is raised from $12,600 to $24,000, a huge chunk of households that normally get the MID would forgo itemizing in favor of taking the standard deduction.

Doing this in one go instead of phasing in any changes — as the Tax Policy Center suggests — could have serious consequences for home prices, with some estimates saying they could fall around 7 percent.

In our hyper-partisan age, both Republicans and Democrats are recognizing that the Mortgage Interest Deduction is just bad policy. With this growing consensus, it doesn’t seem long for this world. Whether the deduction is reformed, transformed, or eliminated entirely remains to be seen. How do you think the MID should change?