DC’s apartment boom continued in 2016. Here’s what that means for your rent.

Cranes at the Wharf. Image by Payton Chung licensed under Creative Commons.

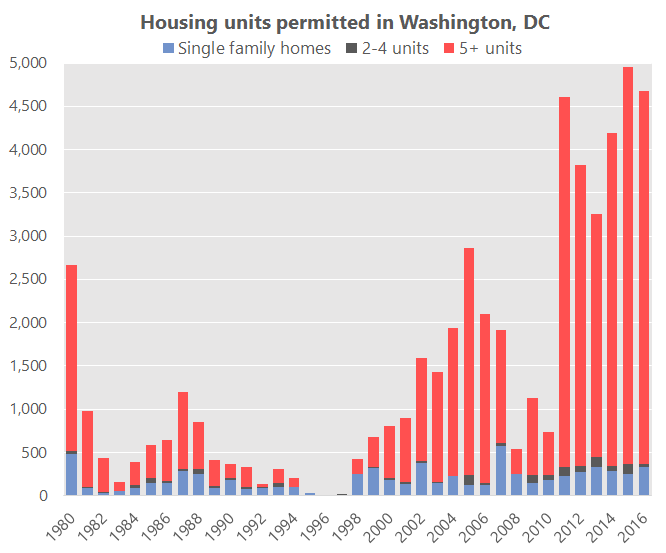

New data shows that DC proper permitted 4,682 units of housing in 2016. This was the second highest number since the Census Bureau started keeping track in 1980 – surpassed only by 2015’s record-breaking amount:

Image by the author.

Robust job growth helped fuel demand for more housing in 2016. The region added 66,600 jobs last year, which constituted a higher rate than the national average.

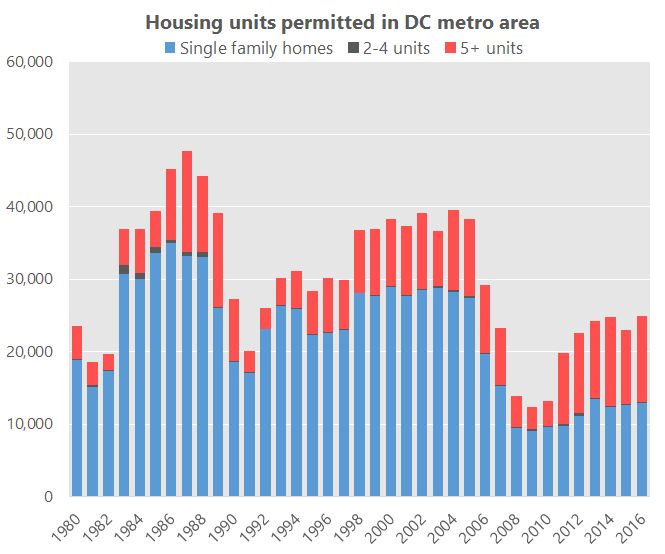

2016 was less impressive for the broader Washington region, which permitted 24,944 units. This is because single-family permits remain well below their dramatic pre-crisis peak:

Image by the author.

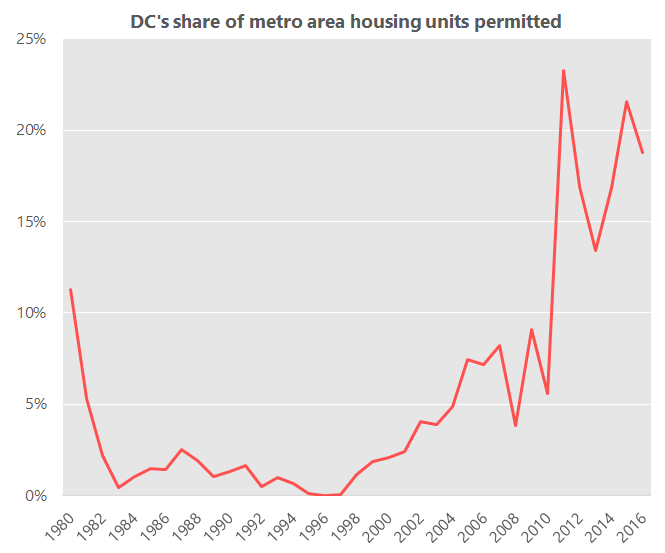

It’s also worth noting DC continued to permit a historically high share of the region’s new housing units…

Image by the author.

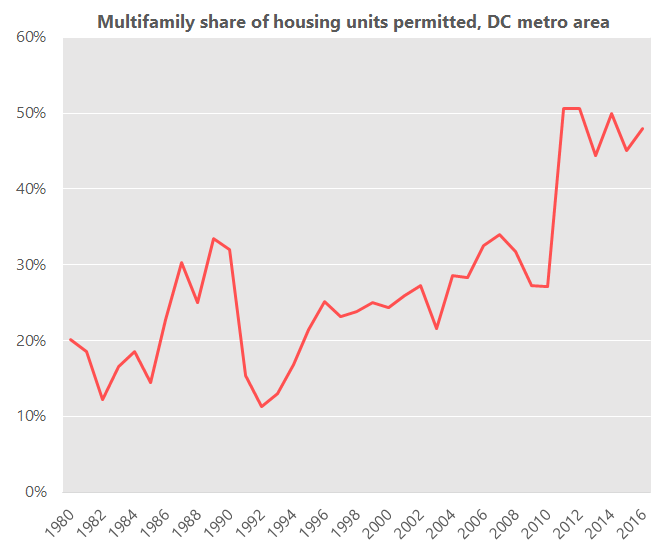

…which is a trend that has contributed to an elevated share of permits for multifamily housing (buildings that have more than one unit) for the entire region:

Image by the author.

Some national context

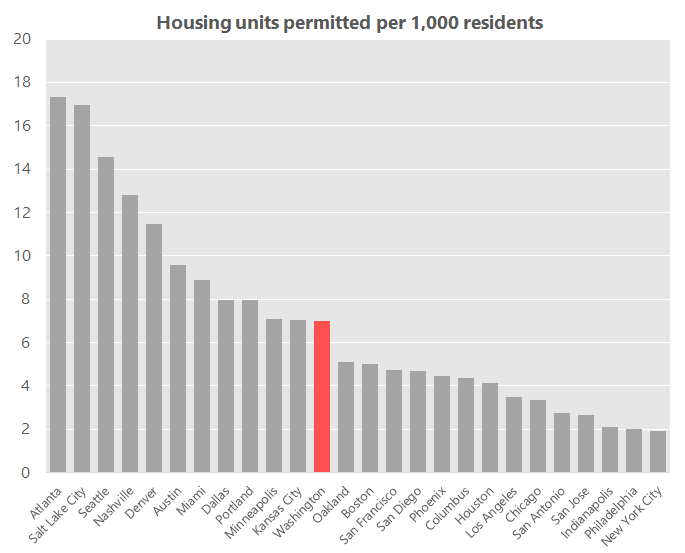

If we scale units permitted by population, we can get a rough estimate of how DC compared to other cities last year. An admittedly nonscientific sample of US cities shows that DC permitted a good amount of permits, at least compared to its high-cost peers:

Image by the author.

A minor caveat for these numbers: apples-to-apples comparisons between cities are difficult. Municipalities often do not have economically meaningful boundaries, and this measure misses important context, like job growth. Still, this is a useful back-of-the-envelope calculation.

In 2016, DC was in line with cities like Portland and Minneapolis. It was out-permitted by the likes of Atlanta, Seattle, and Denver, which have been growing fast in recent years. And DC beat out typically low-growth cities like San Francisco and Los Angeles, as well as Houston and New York City, which are experiencing weak economic conditions and regulatory changes respectively.

{kind=link}

New supply has kept rents at the top of the market under control – for now

Another strong year for permits means that lots of new housing is in the development pipeline. The consensus among real estate experts is that the recent expansion in housing supply has managed to keep DC area rents from spiraling out of control.

December's year-over-year multifamily apartment rent growth in the DC metro region was 2.6 percent, according to real estate research firm Yardi Matrix. This is considerably lower than the national average of 4 percent. They attribute this to DC’s above-average multifamily housing stock growth rate (3.6 percent last year, compared to 2.4 percent nationally).

Freddie Mac’s multifamily research unit agrees. Writing in August, they note that DC is one of a few cities that “saw supply well above their historical averages.” In their view, supply has narrowly outpaced demand recently.

DC’s long-term housing situation is less cheery

An analysis by Axiometrics, though noting that rents are under control now, predicts that supply will fail to keep up with demand in the near future. They write:

…[we project] strong average annual rent growth through 2021. In fact, among the top 120 metro areas in the country, Washington, DC is expected to rank in the top five for average annual rent growth in our forecast window (just behind the San Francisco Bay Area and Seattle).

This demonstrates the need for sustaining a high level of housing production over a prolonged period — something DC has failed to do over the past decade. While our brief run of adding lots of new housing has helped alleviate rent growth, the level of rent is still far too high. Nearly half of households in the city remain burdened by housing costs.

DC and its surrounding areas should make a better effort to encourage market-rate housing production at all viable segments of the market – not just at the highest end. A combination of real estate economics and regulation means that new construction is concentrated in just a few neighborhoods, where zoning is loose and high rents support the costs of erecting large, expensive buildings.

Zoning further-out neighborhoods for cheaper housing typologies, like townhouses and small apartment buildings, could help create downward pressure on rents at the lower end of the market. And of course, all of this should be done alongside a commitment to providing enough below-market rate housing and robust tenant protections.