Can affordable housing create wealth and stay affordable?

Photo by Payton Chung on Flickr.

There is a debate raging in Washington, DC, about how to best balance two equally valid but competing public objectives with the city’s affordable homeownership programs: wealth creation and preservation of housing affordability.

Homeownership is critical to wealth creation for low and moderate-income families. Home equity represents fully 60% of low-income households’ wealth, dwarfing the value of retirement accounts and financial assets. The most important way that households gain equity is by paying down their mortgage; appreciation certainly helps, but in most markets, in most time periods, it is secondary.

But preserving affordability is critical too. In an era of fiscal constraints, local programs are facing increasing pressure to ensure public subsidies are spent wisely and equitably. For example, two key supports for local homeownership, HUD’s CDBG and HOME programs have been cut in real terms by 2/3 and 1/2, respectively, since their peak.

Even for local programs like DC’s Inclusionary Zoning program or public lands dispositions (which rely on “density bonuses” or discounted land prices in exchange for building low-income units), the units produced are still a scarce resource.

Three ways to make homeownership affordable

There are three different schools of thought about the best way to provide affordable homeownership in high-cost markets. The first, the traditional model, is where an owner has no or minimal constraints on profiting. This approach maximizes wealth creation, but does so at the expense of affordability preservation, as typically all subsidies are lost after a short period (e.g. 5 or 10 years).

A second approach, “subsidy recapture,” requires that owners repay the subsidies they received to buy the home, but allows them to capture all the home’s appreciation. (This is not altogether different from Council Bill 20-604, the “Affordable Homeownership Preservation and Equity Accumulation Amendment Act of 2013.”) A third model, “shared equity,” requires that owners leave part of the subsidy in the home to make it affordable to the next buyer, while allowing the first owner to realize a portion of the home’s increasing value.

Shared equity is complex, but it’s increasingly seen as promising because of the balance it offers between the equity gains for the initial homeowner and sustaining the public subsidy in the unit. This is especially significant when trying to preserve the economic diversity of rapidly changing neighborhoods.

How could DC use the expanded Housing Production Trust Fund?

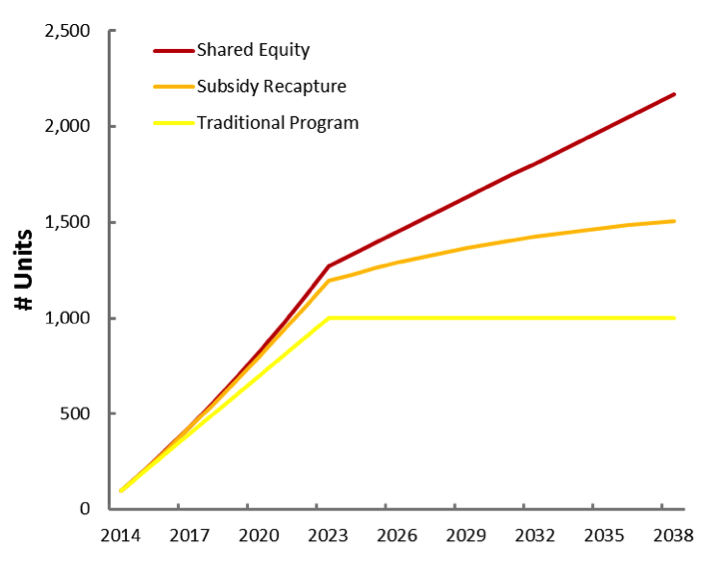

If Mayor Gray wanted to spend all of the $100 million he proposed adding to the Housing Production Trust Fund on subsidizing homeownership for low-income families, how many homes would he provide under each approach? Assuming each home requires $100,000 in subsidy and it takes DC 10 years to deploy the $100 million, the city could, after 25 years, provide 1,000 homes to families under the traditional approach.

Assuming a rate of moving of 6% (the national average for homeowners) and a 5% growth in home prices (reasonable for the District), a subsidy recapture program would provide approximately 1,500 homes, half again as much as the traditional program. Every resale, would return the $100,000 subsidy back to the city, which it could use to reinvest in providing homes in the same manner.

However, $100,000 10 years later doesn’t buy what $100,000 buys today. Think of the changes to home prices in Columbia Heights over the past decade, and now in Petworth.

How many affordable housing units are created through the social equity (red), subsidy recapture (orange), and traditional (yellow) methods.

The shared equity model could provide nearly 2,200 homes during the same time span, for the same public investment. Why is there such a difference between the subsidy recapture and shared equity models? The shared equity approach attaches subsidies to a specific set of homes that resell, while the subsidy recapture approach must subsidize the purchase of new homes with each resale, and housing prices are accelerating far faster than incomes. You can tweak the assumptions that created this figure, but the basic principle holds.

Shared equity and creating wealth

But what do these equity restrictions mean for buyers’ ability to create wealth? Thankfully, we have real evidence from operating programs to inform this. With colleagues at the Urban Institute, I undertook the first cross-site study of seven shared equity programs across the country to examine their outcomes for buyers.

Of the seven programs we examined, upon resale, buyers earned an average internal rate of return of 26% annually. This calculation only measures return from appreciation, not savings gains through paying down a mortgage. These are pretty sizable returns for individuals, and well in excess what people could have made if they had invested their money in the stock market or in a savings account.

Of course if there were no equity restrictions, they would accrue much higher gains, but affordability would be lost upon resale. What then about differences in equity gains between the subsidy recapture and shared equity approaches? Assuming buyers put 5 percent down on a $200,000 home, that home prices rise by 5% annually, and that median incomes increase by 3% annually, the annual rate of return for shared equity program would be 21 percent, and the subsidy recapture would be 29 percent.

What should DC do?

The tradeoff between wealth creation and affordability preservation is real: the more subsidies the first buyer receives, the better off he or she is, and the worse, all else equal, is the second interested buyer. And there are well-intentioned people on all sides of the debate. I don’t presume to have the final word on this debate in DC, but it seems that historically, the city has undervalued future owners while providing outsized assistance to a smaller set of first buyers.

Further, there is no clear justification for letting equity restrictions expire after 5 or 10 years, as is commonly done. If the city wants to provide greater equity gains, it can simply adjust the index used to be more generous.

There is good reason that shared equity models are on the rise nationwide, and especially in high-priced cities like DC. It’s just too expensive for the city to provide traditional homeownership support, and the shared equity model creates more units than a subsidy recapture approach, while still allowing for sizable wealth creation. Washington, DC, has become one of the most inequitable cities in the country. It’s time for robust solutions that will preserve a healthy income mix in the city for decades to come.

The views expressed are my own, and shouldn’t be attributed to the Urban Institute, its trustees, or its funders.