How would Maryland pay for a privatized Purple Line?

Rendering from MTA.

To pay for the Purple Line, Maryland wants to use a form of “public-private partnership,” or P3. Accomplishing this will require some complex accounting.

This form of financing is more expensive than bonds issued by the state, but it may allow the state to borrow money that doesn’t count against its debt limit and free up funds for other transportation projects. Under a P3, a private operator would get those funds from equity investors and lenders.

Maryland has committed $900 million towards the $2.2 billion Purple Line, including $680 million from this year’s gas tax increase. The federal government may contribute an estimated $900 million, and Montgomery and Prince George’s counties will contribute as well. This leaves the state somewhere between $200 and $400 million short.

The state’s debt limit applies to all debt that will be repaid from tax revenue. But the Purple Line will run at a loss, and thus tax funds must ultimately pay for construction. So the Maryland Department of Transportation devised a complex financing structure to get out from under the limit.

Flow of money during operation of Purple Line.

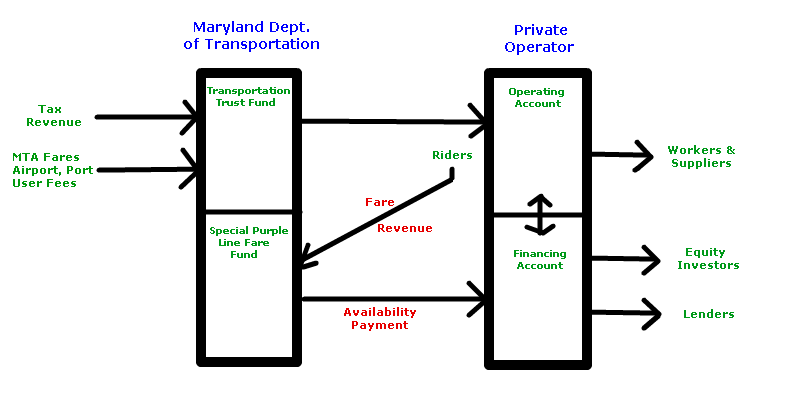

Fares from riders on the Purple Line will go not to the private company that builds and operates it, but into a special state fund. Meanwhile, the Transportation Trust Fund will pay the operator for the cost of running and maintaining the light rail line.

The operator will get a second payment, a so-called “availability payment,” from the fare fund. Its amount will depend on how well the light rail line performs. This money will go to repay the lenders and investors who put up money for construction.

It’s not clear whether this arrangement will pass muster, and MDOT has yet to work out all the details. On September 12, the agency requested guidance from the state’s Capital Debt Affordability Committee on “parameters for structuring the availability payments to avoid classification as tax-supported debt that would impact the State’s debt affordability analysis.”

One issue is whether it’s proper to separate operating costs from fare revenue. There can’t be fare revenue without the state’s ongoing expenditure of tax money to run the Purple Line.

Tax money supports the Metro much as it will support the Purple Line, but Metro does its accounting differently. WMATA subtracts revenues from operating costs and calls the difference its “operating subsidy.” State and federal aid derived from taxes pays for new construction. If the P3 did its accounting like WMATA, MDOT would pay its construction debt with tax money.

A second question involves ‘equity’ investors. About $180 million of the Purple Line’s construction costs is supposed to come from this source. These investors will get compensation from a share of the availability payments, plus operating profits and minus losses.

What will happen if the operations of the Purple Line are not up to snuff, and MDOT cuts its availability payments to the operator? The investors are likely to be large institutions whose managers get bonuses based on each quarter’s returns. They might well push for a cutback on maintenance to generate operating profits in the short term.

That would surely be bad for riders. And would it not divert tax money meant for rail maintenance into repayment of construction debt?

Whether or not it avoids the debt limit, P3 financing will be more expensive than direct state borrowing. A private entity set up to run the light rail line will not have Maryland’s AAA credit rating. The Maryland Department of Transportation also asserts that a P3 would manage the rail line better, resulting in lower construction and operation costs, but it does not promise any net savings. Indirect borrowing for the Purple Line is only wise if the other transportation projects it pays for are worth the money.