Metrobus, MetroAccess fares have declined with inflation

Metrorail fares increased recently in 2003, 2004 and in 2008. What used to cost $1.10 now costs $1.65. Are Metrorail fares growing too fast? Or have fares not gone up enough compared to inflation? Have bus fares kept up with inflation? How has government support of rail, bus and paratransit changed over time?

The recent Metrorail fare increases have kept up with inflation, which has been enough to keep subsidy growth in check. For Metrobus and Metroaccess, fares have not kept up with inflation, and subsidies have increased even after accounting for inflation. Member jurisdictions have occasionally resisted these subsidy increases. Today, that’s leading to service cut proposals.

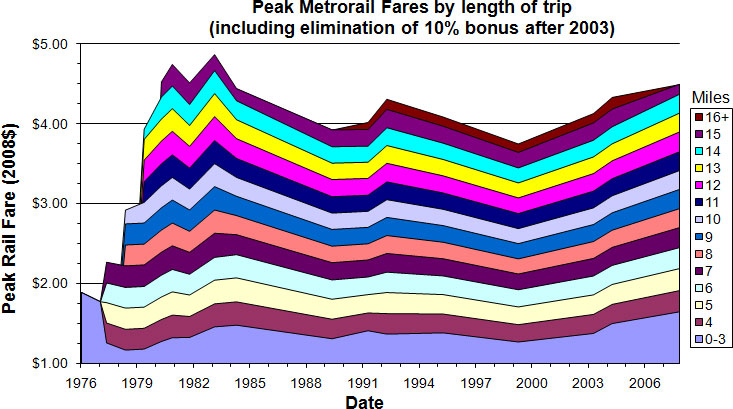

Metrorail:

Metrorail fares have been pretty stable over time. We’ve had a huge increase in ridership since the 1990s, added a lot of new service (more frequent trains, early morning and late night service, longer trains). The WMATA workforce aged and started drawing pensions, as the first Metrorail operators working when the system opened in 1975 must have at least 34 years of service by now. And we’ve endured a few energy crises. Even with all these changes, the real price of Metrorail service for the same distance has stayed pretty constant. This chart accounts for the fact that before 2003, you got a 10% bonus when purchasing $20 or more.* Between 1980 and 2003, bus and rail had the same base fares, and from 1977 to 1980 it it was actually more expensive to ride the bus than to go three miles on the rail.

The other interesting trend is the timing of fare increases. Before 2001, Metrorail fares appeared to increase just after recessions and recede somewhat during boom times. I attribute this to situations similar to the current Metro funding shortfall, where during a recession the local governments are unwilling or unable to increase operating assistance to transit, and rather than cut service to balance the budget, the agency increases fares. Recently, the trend has been a more steady increase.

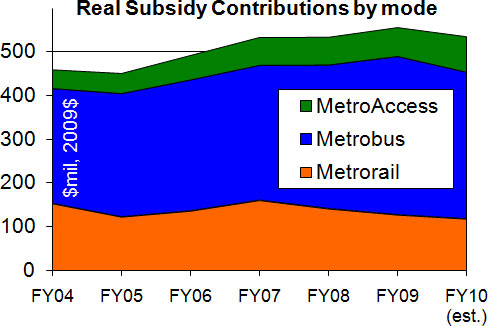

Over the past five years (since FY2004, earliest data available), Metrorail subsidies have stayed flat or declined slowly (about $3.3M less per year) over time after correcting for inflation (2.1% per year real decline). This is likely because fare increases have kept up with added system costs.

Metrobus:

Metrobus fares have declined fairly steadily over time at a rate of about half a cent per year after accounting for inflation. This doesn’t sound like a lot, but over 33 years of operation it adds up to just about 20 cents per ride, meaning that Metrobus fares should be about $1.45-1.55 today to keep up with inflation. Additionally, since MetroAccess fares are based on bus fares, returning bus fares to their historic level would reduce the MetroAccess funding gap. The timing of Metrobus fare increases does not appear as tied to economic trouble as Metrorail.

The long-term Metrobus subsidy trend has grown, at a rate of $14.6M per year (5.5% per year). Service is gradually becoming more expensive for the localities to provide. This is probably driven by real increases in personnel costs as well as the fact that increased ridership cannot be handled as easily with increased vehicle size like with Metrorail. Additionally, as mentioned before, fares have not kept up with inflation, especially over the past five years.

MetroAccess:

MetroAccess fares are based on Metrobus fares, so they also have not kept up with inflation. MetroAccess subsidies are increasing rapidly (13.6% per year). These costs have been growing at a rate of about $5.8M per year since FY2004.

Subsidies:

WMATA subsidies have grown in inflation-adjusted dollars at a rate of $17.1M per year (about 3.7% per year). The two charts to the right show the real percentage growth rate and the contributions to the overall subsidy from FY 2004 to FY 2010. For FY 2010, I knew the Metroaccess subsidy from Board reports, but for Metrobus and Metrorail I had to assume that the decline in real subsidy was shared equally as a percentage of the previous years’ subsidy. This may or may not be correct, the cuts in bus service or rail service may be more severe, which would change the subsidy balance.

Conclusion:

Metrorail fares have stayed generally flat relative to inflation for trips of equal length.** Also, the recent fare increases, combined with other operating revenues, have been enough to keep Metrorail’s government subsidies from increasing. Therefore, it would not make sense to increase Metrorail fares based on an argument that fares have not kept up with prices, or that rail customers are not paying enough for their service.

For Metrobus and Metroaccess, it’s a different story. Based on real subsidy increases over the past five years and a steady downward trend in fares, Metrobus and MetroAccess fares and operating revenues have not kept up with system operating costs. However, such a difference brings up important social equity concerns. Metrobus riders are more likely to be poorer, more transit dependent and less likely to have full time employment (demographic information here). That makes a stronger case for increased government support for those services, as opposed to service cuts or fare increases in order to balance the budget.

I think a reasonable compromise would be to increase bus fares with the rate of inflation, but it’s not necessary and would likely be counterproductive to increase the fares enough to keep the subsidy cost growth rate as low as it has been for Metrorail. Bringing them back into line would mean about a $1.50 bus fare today, which is probably too big an increase all at once. Maybe the fares should increase by 10 cents each time Metro increases rail fares.

Member jurisdictions have occasionally resisted the subsidy increases resulting from inflation. Today, that resistance is driving the proposed service cuts. Service cuts reduce the benefit of having a transit system in the first place. Would it be better if fares kept up with inflation, reducing pressure for service cuts? Maybe with fare increases, there would be money for increased service after the recession is over.

* I was not able to determine when the 10% bonus started. Therefore, I applied it to all fares before 2003 by multiplying them by 0.91.

** Regressions of Metrorail fares for 5, 10 and 15-mile trips with respect to time were not statistically significant at a 95% confidence level.

Sources: WMATA budgets for FY 2007, 2008 and 2009, WMATA Board Reports from January 2009-present, CPI data from Bureau of Labor, and author’s calculations.