Banks find loopholes to deny blacks and Latinos home loans at twice the rate of whites

Image by Jill Slater used with permission.

Here in the Washington region, African Americans are 2.2 times as likely to be denied a home mortgage loan compared to whites, an analysis from Reveal News shows. Latinos are 1.9 times as likely to be denied — even when controlling for factors like the applicant’s income, loan amount, and neighborhood.

This spring, Reveal News published a national analysis of more than 31 million records from the Home Mortgage Disclosure Act. The piece identified Washington, DC as a housing market where modern-day redlining has flourished, in part due to banks using loopholes to avoid scrutiny.

“It’s not surprising at all,” said Kate Scott, Deputy Director of the Equal Rights Center’s fair housing program. “There’s a dual housing market in the Washington region between African Americans and whites.”

The evidence suggests that people of color continue to feel the effects of discrimination in the housing market decades after the 1968 Fair Housing Act and the 1977 Community Reinvestment Act (CRA) were passed. The Community Reinvestment Act in particular has come under criticism for failing in its promise to end race-based discrimination among banks. In an increasingly digital age, the law is focused only on physical bank branches, and its ratings system is highly catered to the institution’s size, service portfolio, and strategic mission.

Reveal found that 99% of national banks inspected under the CRA were granted “outstanding” or “satisfactory” reviews — a measure of success sorely at odds with the underlying data.

Sara Pratt, a lawyer practicing in the areas of fair housing and civil rights at Relman, Dane, & Colfax, observed a similar disconnect during her tenure at HUD’s Office of Fair Housing and Equal Opportunity. “I found virtually no connection between whatever rating they gave and the fair housing and fair lending problems that I observed doing enforcement. None.”

Banks use loopholes to avoid serving communities of color

JPMorgan Chase is one example of a bank that has failed to serve communities of color in DC, turning away applications from blacks and Latinos at starkly higher rates than those of whites. Reveal News found that African Americans were granted just 23 of the 1,119 conventional home purchase loans Chase made in Washington in 2015 and 2016, while Latino applicants received just 35 of those loans.

Chase has largely circumvented federal scrutiny of its lending practices due to its limited brick-and-mortar presence in the District. Despite being one of the biggest lenders in the region, Chase’s sole office in Washington — located across from the White House — does not accept deposits and is subsequently exempt from CRA regulation. Subtle loopholes like these have chipped away at the power of the Community Reinvestment Act to reverse the history of redlining among banks and lenders in the District.

In April, responding to the media coverage of its lending practices, Chase announced it had plans to open 70 new branches in Virginia, Maryland, and the District. The bank has promised to dedicate 20% of the new branches to serving federally-designated low- and moderate-income neighborhoods.

Still, it remains to be seen whether the new branches will improve Chase’s record of lending toward groups of color. “The devil is in the details,” Kate says, since banks don’t reliably offer the same types of services at every branch.

Whites have an easier time getting lending services and loans in Petworth

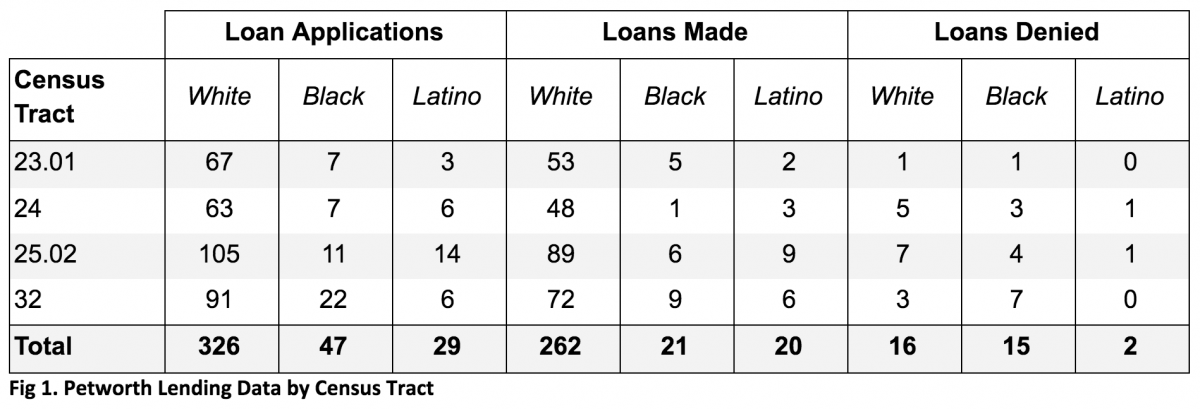

Reveal’s analysis includes an interactive map that lets users explore mortgage-lending data for any community across the country. (Access the full map here to find data for your neighborhood.) A closer look at the Washington region shows that in Petworth, a historically redlined neighborhood of DC, white residents not only had an easier time accessing lending services but had their loan applications approved at a much higher rate than black applicants.

Between 2015-16, as many as 262 home mortgage loans were awarded to white applicants in Petworth, compared to 21 loans awarded to African American applicants and 29 loans made to Latinos. The racial disparity clearly leans in favor of white residents in this neighborhood, despite the fact that whites make up just 20% of its population.

Of the total home mortgage loans originating in Petworth, 80% of white applications were approved while only 44% of those from African Americans were.

Source: Reveal analysis of Home Mortgage Disclosure Act data, US Census Bureau.

Petworth is perhaps a prime example of the way gentrification and rapid demographic change are shifting the housing landscape in DC. In an area where upwardly-mobile, white newcomers are entering the housing market, single-family homes that in prior decades might have been renting are now swiftly going up for sale. As a result, more home purchase loans are applied for overall, and racial disparities in the housing market become more pronounced. “What is actually going on there is probably even more intense than what the data is showing,” said Kate Scott.

Though Reveal’s analysis shines a light on the racial disparities in the Washington, DC housing market, ours is just one of 61 metro areas where people of color were statistically more likely to be denied a home mortgage loan than whites.

According to Sara Pratt, it’s likely that every city—including Washington—requires “more work to be done on making sure that the conventional lenders are present, looking for, and working with neighborhoods that have lots of single family houses but that do not have access to conventional lending or conventional banking services.”

We’d like to hear from you. If you live in the greater Washington area, have you faced challenges securing a mortgage to purchase a home?