DC has a program to help first-timers buy a house, and it may start giving more aid

DC has a program for helping people buy houses, but the money it awards doesn’t line up with how much houses in the city actually cost. The program might start awarding more money soon.

Photo by C.E. Kent on Flickr.

Programs to support first-time home buyers help spur economic security and neighborhood stability across the US. In Washington, the Home Purchase Assistance Program has been the key tool for the District to support first-time homebuyers.

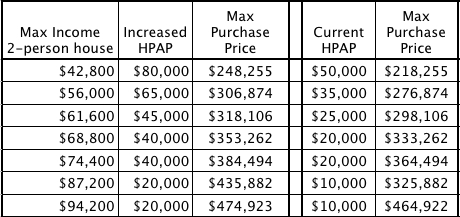

On January 7th, the DC Council held a hearing to consider raising the maximum amount applicants can receive, from $50,000 to $80,000.

The proposed increase in loan amount would increase HPAP buyers’ purchase power and give them access to more homes on the market. The figures below are based on 38% front end ratio (the proportion of monthy income that would go to the full cost of the mortgage) and a 5.5% interest rate, so maximum purchase prices could be higher. Tables from the Housing Advocacy Team.

HPAP helps people jump one of home buying’s biggest hurdles

When someone buys a house, they take out a regular mortgage loan from a traditional bank for the bulk of the home price. HPAP augments that money by providing what’s known as a “second trust loan.” HPAP money can also go toward a down payment, and the program offers an additional $4,000 to help with closing costs.

The actual amount that the borrower is eligible for is based on their income, with lower income households eligible for more assistance. Those receiving the highest loan amounts make 50% of the area median income or less. Participating owners receive both pre- and post-homebuyer education, and they pay back the second trust loan with zero interest starting in the fifth year of their mortgage.

Saving for a down payment is often the greatest barrier to owning a home. Many people already pay high monthly costs in rent and could afford the monthly cost of a mortgage and upkeep, but cannot also save tens of thousands of dollars towards a downpayment. In fact, according to the real estate website Trulia, it is 27% cheaper to buy in DC than it is to rent. Having a significant downpayment also lowers interest rates and monthly mortgage costs for the length of the loan.

A greater award amount would help buyers in a tougher market

Over the last decade, the maximum amount of money that HPAP awards a buyer has fluctuated greatly. That variation hasn’t been based on housing prices, but rather DC’s budget and spending pressures.

In 2008, the award amount was capped at $70,000. But when the recession hit, federal and local resources shrank, and the award amount dipped to $40,000 per purchase. While that rose to $50,000 in 2014, that jump paled in comparison to the rapid increase in the cost of buying a home here.

With HPAP’s limits being what they currently are, most low-to-moderate income buyers could only afford homes under $300,000. According to Zillow, the median home price in DC right now is $502,600, and on average, between 2012 and 2014 there was 4.7 percent reduction in the number of condos and homes affordable to most HPAP borrowers.

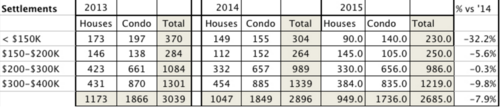

MANNA, a nonprofit that has helped DC residents purchase homes for decades, crunched some of the numbers and put them into to charts:

As purchase prices have increased, the number of houses at prices affordable to HPAP buyers has dropped.

Should the DC Council increase HPAP’s maximum award amount, houses in the $300,000-$400,000 range would be available to a lot more prospective buyers.

Thursday’s hearing demonstrated wide interest in changing the award amount. Housing and Community Development Committee Chair Anita Bonds chaired the hearing and was joined by Councilmembers Nadeau and Silverman. All of the public testimony supported the increase, and Polly Donaldson, the Director of the Department of Housing and Community Development, which manages the program, expressed interest in increasing the award amount.