Cuts threaten successful homeownership program

Photo by AKZOphoto on Flickr.

Affordable housing in the District is disappearing, and programs to help low- and moderate-income residents afford housing in DC are dwindling. One of the affordable housing programs at risk in this year’s budget, thanks largely to federal budget cuts, is the Home Purchase Assistance Program (HPAP), which has helped 13,000 low-income renters become homeowners in DC.

HPAP has a track record of success, a credit to the non-profit housing organizations that administer the program. In addition to financial assistance, HPAP recipients also receive intensive financial and homebuyer education, preparing them for the responsibilities and challenges of homeownership.

Even through the housing crisis, HPAP recipients only have a 2% foreclosure rate. And HPAP has helped maintain diversity in changing neighborhoods like LeDroit Park, Columbia Heights, and Logan Circle. HPAP assistance has been a key tool in supporting new homeowners in the District, even as the city has lost the majority of its low-cost rental and ownership housing since 2000, according to the DC Fiscal Policy Institute.

How does HPAP work? HPAP is the District’s homegrown downpayment assistance program which provides up to $44,000 for first-time, low- and moderate-income home buyers. HPAP acts as a second mortgage. Recipients begin paying their loan down starting in year five of owning their home and make monthly payments over a 40-year period instead of the traditional 30-year period, making the payments more affordable. As HPAP recipients repay their loans, the city recoups the cost, which currently generates $2 million in repayment every year.

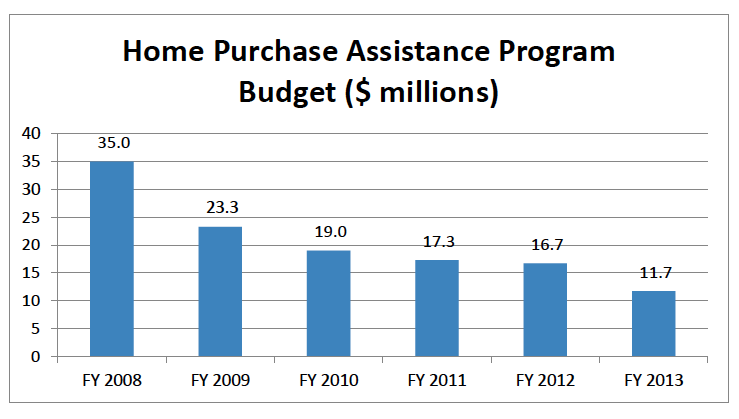

Although beloved by politicians and residents alike, HPAP has dwindled since 2008. The program in FY13 is slated to be only a third of its size only five years ago. As a result, the number of people who can use the program has fallen. And this year, the decrease will impact about 100 families. According the DHCD, last year the program served 246 families, next year it will serve around 150.

The city has used federal funding to maintain the HPAP program, relying heavily in recent years on stimulus dollars, but this year, federal funds are not available to fill the gap. The federal Department of Housing and Urban Development’s grant programs that have also funded HPAP also dwindled; its HOME program shrank 37% in 2012, and its Community Development Block Grants (CDBG) dwindled by 12%.

Also, the 2010 Census made DC is eligible for less CDBG funding, since the city has fewer high poverty areas than in previous years. All of these combined losses have left few funds available for housing programs like HPAP.

HPAP budgets have decreased substantially since FY 2008.

In April, more than a dozen HPAP recipients attended the DHCD budget oversight hearing to advocate for the program that has helped them become District homeowners. Attendees highlighted the diversity of residents impacted by the program.

Elizabeth Palmberg purchased her home with an HPAP loan, only to be diagnosed with lymphoma soon after. She has been able to afford her mortgage despite her health struggles; “the HPAP program helped me to be able to still buy my condo, and now every month as I write my mortgage check, I am grateful to be building equity which will give me stability against shocks that life might send my way in the future.”

Bernice Joseph was able to purchase her home in Logan Circle in 2002 and has no plans of leaving the neighborhood. She loves the convenience, and believes that HPAP has had a huge impact on her family and her educational opportunities. “Without this program I do not know where I would be. But I do know I would not be in my neighborhood, the one that is so dear to my heart, the one where I have put down roots, and the one where I have lived for the past 21 years. I have raised all four of my kids in DC. Without the stable price of my mortgage, I would not be able to afford to go back to school. I definitely could not afford my classes if I had to pay market-rate rent.”

The value of homeownership of course extends beyond the individual. Homeowners pay property tax back to the city and provide an anchor for communities. Homeownership is an indicator of success for families and kids across the country and one of the most important wealth-building tools in our country, especially in communities of color and low-income communities. A 2003 study found that housing wealth accounted for 77% of all low income household’s wealth.

HPAP has supported District residents and communities by encouraging homeownership, neighborhood stability, and equity building. This year, the program will become even weaker after years of reductions. The DC government should encourage residents to become homeowners, to invest in their communities and themselves by supporting the HPAP program with local funds.

Sarah Scruggs contributed to this blogpost, which can also be found at www.housingforallblog.org.